Accepting default is Europe's only option

The only way to escape the current crisis is to default on much of the debt that caused this crisis in the first place: private credit lent to households that financed the bubbles in housing and shares since the early 1980s, writes Steve Keen.

The dramatic falls in share prices of Greek debt-laden French banks overnight (10 August) highlights just how closely tied the current market chaos is to the world’s worsening debt woes.

Market crashes like that of 2007-08, when Wall Street’s S&P500 index fell over 50% in 15 months, aren’t normally followed by a repeat performance like the last two weeks.

Even the long slump of 2000-2002, when the S&P 500 fell from 1500 to 800 points, was followed by a five-year boom that pushed the index back to just above its 2000 high.

That is evidence enough that this isn’t a new crisis: it’s a continuation of the old one. The only difference is that this time, governments and the media are focusing on the levels of government debt.

But the real culprit remains the one they briefly shone their torches on in 2007: the level of private debt.

Government bailouts of the private banks shifted some of this debt onto the public account, and desperate stimulus packages to avert a depression created yet more public debt.

But the level of private debt built up chasing Ponzi schemes in shares and housing was so great in the lead up to 2007-08 that its dynamics are still what is driving the global economy back into recession.

The difference today is that private debt is now falling, and as it falls, it is sucking aggregate demand out of the economy. This in turn is causing governments to run fiscal deficits, as tax receipts fall and welfare payments rise.

That gives us one factor reducing aggregate demand — the private sector — and another boosting it — the government. The end result is a slump, but not so nearly as deep a slump as there would be if the government “balanced its budget”.

Unfortunately, politicians are responding to this as they always do — by seeing the government budget as the problem, and ignoring what the private sector is doing.

They therefore compete at being “hairier-chested than thou” in pledging to return the government to surplus.

But the real cause of the crisis is not the government’s balance sheet, but the private sector’s. Government attempts to fix their own balance sheets while the private sector is also trying to reduce debt results in two forces dragging aggregate demand down, which compounds the problem of deficient aggregate demand. A deeper slump is likely to result.

The only way out of this crisis is to dishonour much of the debt that caused this crisis in the first place: the private credit lent to households that financed the bubbles in housing and shares since the early 1980s.

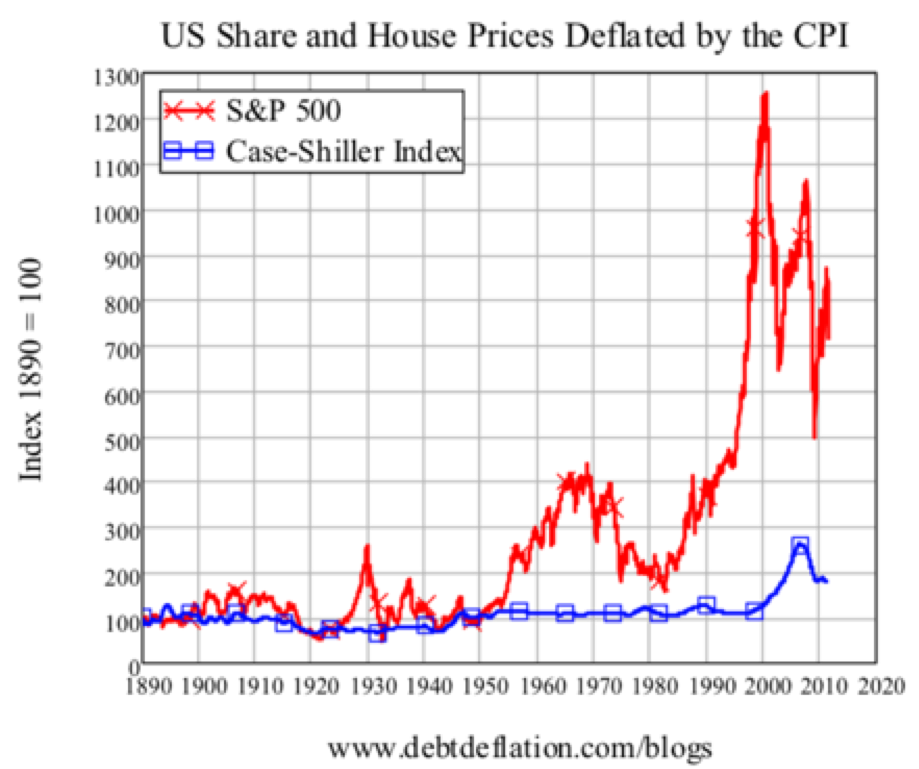

This bubble is so big that future generations will marvel at our inability to see it: share prices have risen sixfold compared to consumer prices since 1980, and house prices have tripled.

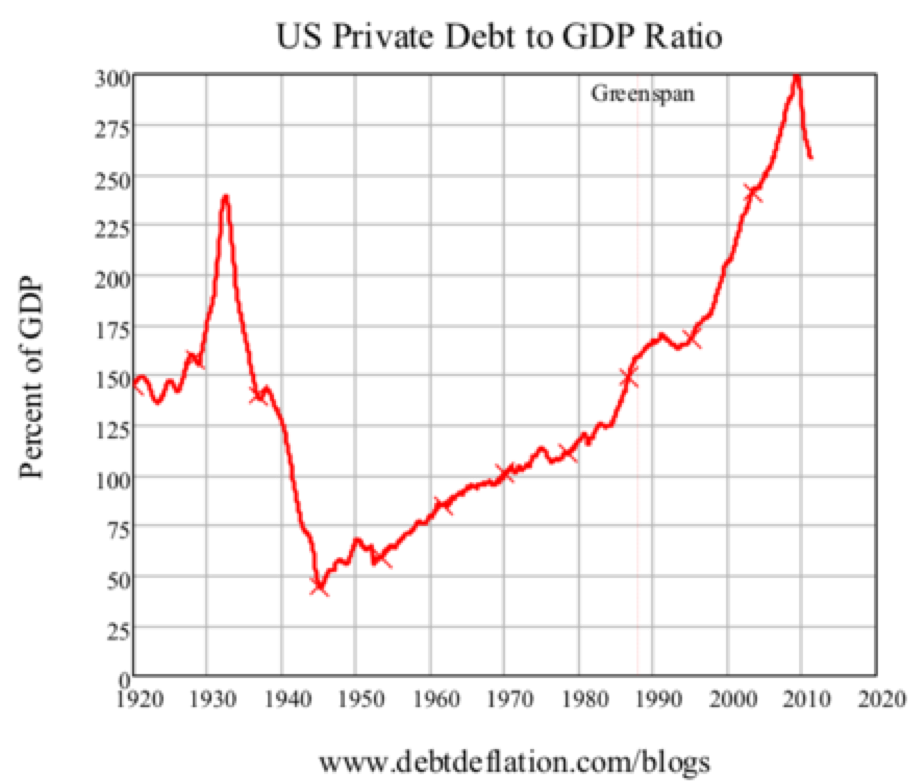

The debt is equally massive—again, future generations will be dumbstruck that we didn’t notice this exponential blowout in private debt, and that we couldn’t understand that the crises since 2007 were caused by this explosion of private debt faltering and then going into reverse.

Given our blindness to cause and effect, a number of avoidable crises are now likely to unfold. The Eurozone is likely to collapse, since no country in it — except possibly Germany — can avoid default if the terms of the Maastricht Treaty are enforced.

These treaties prevent the European Central Bank from actually behaving like a central bank, and funding the deficits of its nation states, if they exceed 3% of GDP. Instead each European nation has to issue bonds to cover the difference, and since it is now so enormous—often above 10% of GDP—markets doubt their capacity to finance that debt. The result is a blowout in bond rates that makes default a self-fulfilling prophesy.

There is a simple solution to the Eurozone’s fiscal problem: the ECB should actually behave like a Central Bank and finance the debt of its member nations, as economist Yanis Varoufakis suggests.

If it issued the bonds — rather than each country — then the aggregate strength of the Eurozone would be behind the bonds, and rates would remain at the level the US currently faces. Almost all European nations could then fund those bonds easily — the only problem child would be Greece.

But the Eurozone, the US, and the rest of the OECD still face the problem of a private sector reducing aggregate demand by deleveraging.

We’re seeing this now in Australia, where a household sector that is more indebted than US households and paying much higher interest rates has stopped spending, resulting in major retailers like David Jones reporting a 10% fall in sales.

Rising unemployment can’t be far behind, despite unprecedented exports to China, as demonstrated by today’s slight increase in the jobless rate to 5.1%.

The only solution to this problem is to dishonour much of this debt — since it was irresponsibly lent in the first place. The private and merchant banks that issued that debt would be sent into receivership, and that would cause substantial economic pain. But it would be a far less long-lasting pain than that of a decade or more of private sector deleveraging.

Steve Keen is Associate Professor, School of Economics and Finance at the University of Western Sydney.

Originally published on ![]() . Published under a Creative Commons Attribution-No-Derivatives 3.0 license.

. Published under a Creative Commons Attribution-No-Derivatives 3.0 license.

Image top: Jo-Sau.

{jathumbnailoff}