NAMA: An activist's guide

On Sunday, 13 November, as part of the DIY Skillshare Festival in Wesley House on Dublin's Leeson Street, Conor McCabe and Mick O'Broin will lead a workshop on NAMA - how it works, what's wrong with it, and and what possibilities there are to fight back against the State's biggest property speculator. Below, O'Broin presents an activist's guide to the agency described by Enda Kenny in 2010 as "a blank cheque to bail out the banks".

Why NAMA was set up

What NAMA basically does is to take loans (good and bad) related to property development and land speculation with a view to development. These loans are taken off the banks. Banks got into big difficulties as a result of the financial crisis. They had ‘liquidity problems’, meaning they couldn’t get money themselves. A banking crisis can lead to a general economic crisis. By taking the riskiest assets it is thought the banks can become viable again because there is less uncertainty:

“Replacing these property loans with Government Guaranteed Securities [aka NAMA bonds] will remove uncertainty about the soundness of banks’ balance sheets and make it easier for them to access funds in the international financial markets. Banks cleansed of risky categories of loans will be free to concentrate on their core business of lending to and supporting businesses and house holds” (NAMA, 2010).

So NAMA attempts to do two things: (1) ease the overall financial crisis by stabilising banks; (2) provide liquidity (cash) to banks so they can start lending again, hence stimulating investment.

So far NAMA has not been successful:

“NAMA has failed to deliver on a primary aim, to create liquidity in the Irish banking sector, which needed further recapitalization and nationalization” (Kitchin, 2010).

In other words, the banks have not been stabilised, we have to keep throwing money at them, and they are not lending.

Loan transfer breakdown

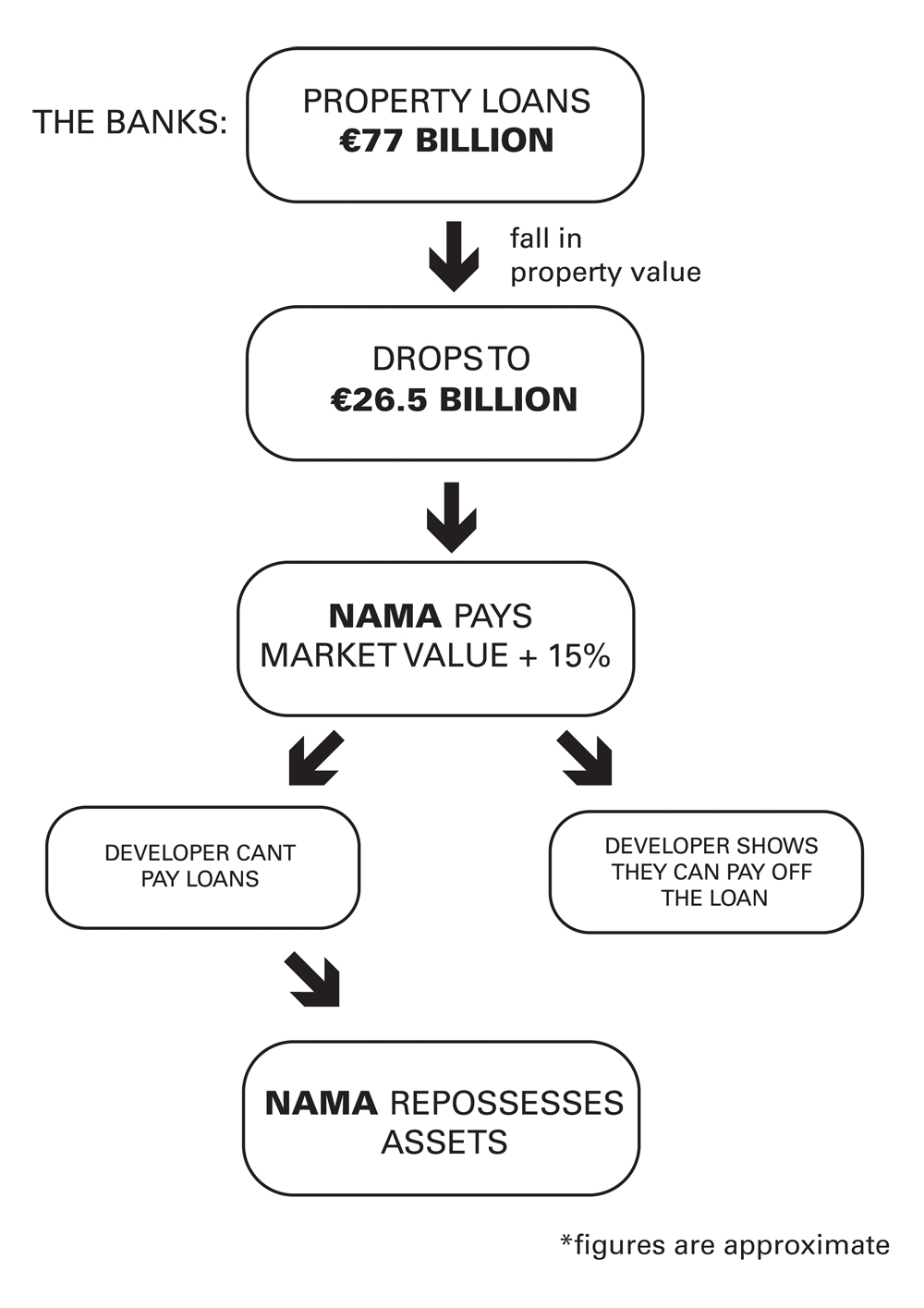

We can break down a bit what was involved in the transferring of loans to NAMA. NAMA identified the property-related loans the participating banks had on their books. Initially this related to loans of over €5 million issued before December 2008, but apparently this has been changing over time. These loans amounted to €77 billion, of which €49 billion are ‘land and development’ and 28 billion are ‘associated loans’ (loans backed by commercial investment properties). This amounts to between 14,000 and 15,000 loans (NAMA, 2010).

NAMA provides the banks with money in return for the loans, hence providing the banks with liquidity. NAMA does not pay the full original value for the assets. This is because their value has decreased hugely due to the property crash. NAMA pays the estimated current value of the loans plus an additional 15%, which is supposed to represent “long-term economic value”. This 15% mark-up is one of the most controversial aspects of NAMA because the idea that the long-term value of property will amount to a 15% increase over the next ten years, at a time when property prices are collapsing, is highly implausible. Altogether, NAMA has paid 30.5 billion to banks (NAMA, 2011).

Alan Dukes (chairman of what was Anglo Irish Bank, now merged with Irish Nationwide and renamed the Irish Bank Resolution Corporation) recently indicated that NAMA may require a further €75 billion to take on additional loans. While NAMA denies this, the continuing banking and property crises means that NAMA may indeed end up increasing its spending.

Alan Dukes (chairman of what was Anglo Irish Bank, now merged with Irish Nationwide and renamed the Irish Bank Resolution Corporation) recently indicated that NAMA may require a further €75 billion to take on additional loans. While NAMA denies this, the continuing banking and property crises means that NAMA may indeed end up increasing its spending.

NAMA doesn’t give the banks cash directly. NAMA gives them NAMA bonds, or Government Guaranteed Securities. These are like IOUs. The banks give these to the European Central Bank in exchange for money. Then NAMA, at some stage, (presumably before 2020 when it is supposed to wind up) will pay the ECB back the money.

NAMA initially claimed that it would generate €5.5 billion in profit by 2020. The idea was that NAMA will generate money from “performing loans” (loans that are being paid off). For non-performing loans, as explained in more detail below, NAMA can take over the related property or commercial assets. These can also generate money, typically by selling them. More recently NAMA Chief Executive Brendan McDonagh declared that the organisation now hopes to generate €1 billion over its lifetime. In 2010 NAMA lost €1.1 billion.

In terms of where the assets transferred to NAMA come from: 67% of assets are in the Republic of Ireland; 6% in the North; and 21% in the UK. About 36% of assets are land; about 28% are development loans; and about 36% are associated loans (Kitchin, 2010). The breakdown by bank is as follows: AIB-€24bn; Bank of Ireland - €15bn; Irish Nationwide - €0.8bn; Anglo-Irish Bank - €28bn. I think ESB is also participating but I’m not sure to what extent.

To sum up at this point, NAMA effectively gives the banks 15% above what the assets were worth at the time of purchase and then takes the assets wholesale off the banks’ hands. Property prices have continued to fall dramatically since 2009, so at this point NAMA (i.e. me and you) has massively overpaid for the assets. NAMA’s claim that it will make the money back is based on the prediction that property value will increase by 10% over the next ten years (NAMA, 2009). In other words “to recover the state investment the property market will need to be re-inflated” (Kitchin, 2010).

What happens next?

Once NAMA has acquired the loans its job is to manage them. This can go two ways. Borrowers have to submit a 3-year business plan to NAMA within 30 days of loan transfer (NAMA, 2010). If they are approved, all continues as if it was a normal bank; the developer continues paying interest as if it was dealing with a bank, and will eventually pay off the loan.

However, if NAMA considers that a specific loan will not be repaid it can take action by appointing a receiver to take control of the property. It can also seize other assets supporting the loans (residential property, commercial investment properties, shares etc). This is often referred to as “enforcement action”. NAMA then has six options: sell; lease; hold; develop; manage/maintain; demolish. NAMA can make funds available (solely or as a joint venture) for developments to be completed. If the property is, say, a shopping centre, the receiver will run this with the objective of maximising profit. Receivers often run businesses in a ruthless fashion - for example firing staff and reducing wages. It would be interesting to see if this is occurring in commercial activity under NAMA. If the properties are to be sold a receiver can also take charge of that process.

According to Simon Carswell, NAMA has reviewed business plans for 91 of the top 180 borrowers and enforcement action has been taken against 27 of these.

NAMA governance

NAMA is a Special Purpose Vehicle and is a separate legal entity set up by the State. It is 49% State owned and 51% private. However, my understanding is that AIB and Bank of Ireland make up most if not all of the private investment. AIB is around 99% state owned. BoI was about 34% state owned, but state share has been reduced to around 15% of late as a result of new private investment. The structure is such that NAMA’s debt is kept of the State’s balance sheet. This is basically a trick which the EU goes along with because, on the basis of the Stability Pact, countries aren’t supposed to be generating the kind of debt Ireland has been and this is a way to make it look like we’re not. However, according to a Namawinelake article, the NAMA bonds are being considered as State debt by Standards and Poor and other International Credit Ratings Agencies. As such, NAMA debt is one of the reasons Ireland has had its credit rating continually downgraded, which is why we’ve ended up in the EU/IMF bailout.

On paper NAMA has decision-making autonomy, although people don’t take this too seriously because the government has a veto.

Importantly, NAMA isn’t subject to the Freedom of Information Act. This means that little is known about its operations. In mid-September, the Commissioner for Environmental Information, Emily O’Reilly, ruled that NAMA is a public authority under the terms of the Environmental Information Regulations, which may mean that more information will come available about its workings in future. For now, though, its operations are almost wholly opaque.

The running costs for NAMA in 2010, according to the agency itself, were €46 million (NAMA, 2011). Between NAMA and the NTMA (National Treasury Management Agency), its parent organization, there are 17 people employed on over €200,000 a year, 14 of whom earn in excess of €250,000.

The Irish State: the world’s worst property speculator?

NAMA crystallises the most grotesque and dangerous dynamics at work in Europe today. First of all, it socialises risky assets, leading to losses for ordinary people. This means public debt has increased and reached unsustainable levels, a fact which the State is responding to by attacking public services, working conditions etc. NAMA has exaggerated this socialisation of losses by overestimating the value of the assets, through its ludicrously inflated estimations of long-term economic value.

Secondly, while the NAMA Act includes ‘social and economic development’ as an objective, this has been ignored by NAMA. NAMA has instead pursued limited economic objectives, meaning it perceives its assets in pure economic terms, despite the fact that NAMA’s assets are our homes, our cities and our countryside. This ignores possible social uses. Many of these assets are idle or being run at a loss (like the hotels). They could, and indeed should, be used by citizens for social and public projects. NAMA’s narrow economic remit also means the cities and country we live in will continue to be over-determined by a short-term and property-obsessed view.

Finally, and perhaps most disturbingly, NAMA ties together the public interest and property-led growth (and as such credit). In recent decades ordinary people have gained an interest in the economic system by becoming property owners and indeed property speculators, thanks to easy credit and low interest rates. NAMA goes one step further because it links the State itself to the property market and to speculation. The property market needs to undergo a dramatic increase in order for NAMA to recoup its money. This has a chain effect: for property to go up, easy credit needs to be available, for this we need strong banks, this requires more support to the banks at the expense of public services etc; easy credit makes house prices go up, which means we have to borrow more and more. And so on.

More generally, NAMA is a key part of the set of processes through which the very distinction between public and private has disappeared. In Ireland today we have something akin to state-capitalism: the State controls virtually the entire banking sector, plus a large amount of the property sector. Through NAMA it is indirectly running everything from pubs and hotels to apartment blocks. In this context appeals to the State to protect the interests of citizens and workers are naive. All our basic assumptions about politics are being put to the test.

Fighting NAMA means fighting the financialisation of life, indebtedness, and property-lead growth. It means fighting the collapse of the public and the expansion of capital.

Fighting back: life after property speculation

One of the difficulties in fighting back against NAMA, and this is probably true of the crisis in general, is the overwhelming nature of the amount of money involved. This is no coincidence; NAMA’s first line of defense is secrecy and mystification. So finding, gathering, analysing and sharing information on NAMA is one way of attacking NAMA. Some resources for those who want to undertake further research on NAMA are available here.

Second of all NAMA has a number of physical and material manifestations. These are points at which we can intervene. The offices of NAMA are at the

Treasury Building, Grand Canal Street, Dublin 2, Ireland. NAMA, as mentioned, has two sets of assets. Those which have been placed into receivership and hence which NAMA has more direct control over can be seen here.

NAMA’s overall (estimated) list of assets is available here.

But what demands and analysis should we advance? In other words, what would constitute a radically egalitarian and democratic approach to NAMA?

The first thing to point out is that if NAMA’s assets are not sold then we lose out in the sense that NAMA accrues more losses which are paid for by the State. This is not an unfortunate side-effect; as already argued, one of the main features of NAMA is to weave together the State and property speculation.

So this could mean that any action against NAMA is represented by the media as an attack on the national interest.

That said, the following points should be the point of departure for the struggle against NAMA:

- We reject the premise of NAMA: socialising losses

- We reject the linking together of the State and property speculation in any form

So if we reject property speculation, which is one system for valuing and organising property, and we reject the socialisation of losses, what alternative do we propose? My argument is that we can advance an alternative approach to the use of properties (and other assets), one in which social and cultural value would be emphasised above economic value. This would take place through the socialisation of resources, rather than losses. We could directly show how NAMA properties can be given another use, rather than being sold-off on the cheap.

There have already been a number of attempts to give alternative uses to NAMA buildings. Limerick City Council has apparently been facilitating artists using NAMA buildings. The Complex theatre space in Smithfield (Dublin) is located in a NAMA property. However, while it is positive to see NAMA buildings being used for art and culture, we also need to question the political implications here. It is well known that art and culture play a key role in urban regeneration, property speculation and gentrification by revitalizing areas. If alternative uses are simply ways to increase the value of NAMA buildings then we reproduce the logic of speculation. This doesn’t mean it’s ‘wrong’ to have art spaces in NAMA buildings, but it does mean that doing so does not in itself break with the logic of NAMA - namely the socialisation of losses and State-led property speculation. There is a second issue here, evidenced by the case of the Complex. When the building which houses the Complex was repossessed by NAMA, the agency issued an eviction order with a view to renting the property to a Tesco Express. Again this indicates NAMA’s inability to see anything beyond the speculative value of property.

However, the Complex has been challenging the eviction and the use of art/culture under the banner of property speculation. One element of their strategy has been to highlight the “social dividend” promised in the NAMA legislation, and also in the Labour and Fine Gael election manifestos. This strategy represents a way for social movements to resist the logic of property speculation and to make a legitimate claim to another type of value. Such a strategy could be developed into a general demand that the NAMA legislation be changed such that all assets are fully open for public and social uses.

In this regard we can show how resources can be socialised in practice, by direct action. Social movements could begin putting existing NAMA resources to social uses.

To facilitate this we should also be putting pressure on NAMA to become a more democratic and transparent organisation by (a) making all information publicly available and (b) developing genuine, participative and democratic engagement with the citizens. I think these demands would most effectively be pursued through a broad strategy including direct action.

It would also be interesting to investigate if NAMA can default on its bonds. This would be effectively a State default and the European Central Bank would be picking up the tab, so it’s no doubt complex. But so is paying back the kind of debt the State has been generating through the transfer of wealth to the banks.

References

NAMA. 2011. Annual Report and Financial Statement 2010. Available here.

McDonagh. 2011. Breandan McDonagh, NAMA Chief Executive, speech at launch of 2010 annual report. Available here.

NAMA. 2010. NAMA: A brief guide. Available here.

NAMA. 2009. Draft Business Plan 2009. Available here.

Rob Kitchin. 2010. ‘Property Crises in Ireland and NAMA’ presentation for the Provisional University at Exchange Dublin, 7th of February 2010.

The DIY Skillshare Festival runs from 11-13 November in Wesley House, Leeson Street, Dublin. View the programme here. {jathumbnailoff}